Kyla Scanlon’s smart: The vibecession and the election

Will voters’ bad vibes elect Trump? Scanlon’s vibecession concept by the numbers.

Source: twitter.com/kylascan

Hot takes (some even evidence-based)

2024 is not a typical “it’s the economy, stupid” election.

The economy is strong. Inflation and unemployment are low.

But, Americans are still gloomy about the economy. Consumer sentiment remains below average.

Kyla Scanlon calls negative feelings about the economy in the absence of an economic recession a “vibecession”.

Trump should be winning this post-vibecession election. No major party has failed to win back the White House with consumer sentiment as low as it is now.

Harris can still win because Trump won’t focus on voters’ economic discontent.

No one on team Trump is brave enough to tell him: “it’s the economic vibes, stupid candidate”.

Read on for my Scanlon-Sayeed rules defining vibecession and vibecovery.

Vibecession: Scanlon coins the concept

Kyla Scanlon coined the word “vibecession” in June 2022:

“Vibecession - a period of temporary vibe decline where economic data such as trade and industrial activity are relatively okayish”

Scanlon recently elaborated:

“A vibecession is a disconnect between consumer sentiment and economic data. Most of the time it stems from things … that aren’t showing up in the way we traditionally measure economic success, like GDP [Gross Domestic Product].”

Vibecession: It IS unusual

This post is a long read. I define Scanlon’s vibecession concept in numerical terms.

Before diving into heavy going, let’s begin by imagining Tom Jones singing his 1960s hit song about a love recession updated by me to be about vibecession.

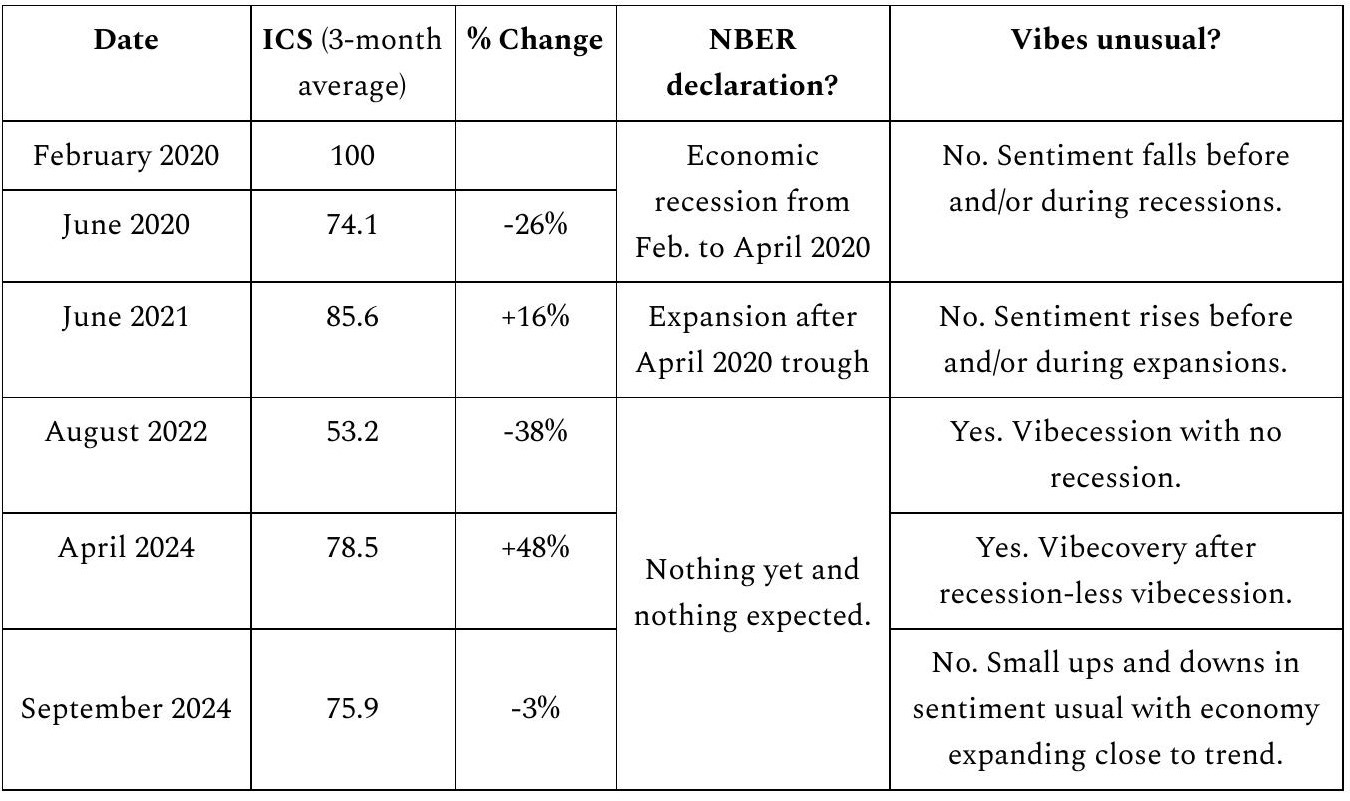

It's not unusual to be sad When times are bad. It’s not unusual for buyers To be down when recession comes. You'll find it happens all the time. But, when I see ICS down with jobs still high and when I hear NBER not saying anything, That is unusual and called vibecession time.

Refining the vibecession concept with Krugman’s help

In early 2024, New York Times columnist Paul Krugman credited Scanlon for inventing the concept and lamented:

“a disconnect between economic perceptions and economic reality … a vibecession … The economy isn’t actually bad — in fact, it’s in remarkably good shape… Yet somehow there’s a pervasive sense that the economy is bad”

Last month, Professor Krugman commented:

“The widely cited University of Michigan survey of consumer sentiment continues to show a more negative view of the economy than one might expect given fairly low inflation and low unemployment.”

With what Scanlon and Krugman wrote in mind, consider the following:

The National Bureau of Economic Research (NBER) Business Cycle Dating Committee has identified 11 American economic recessions since 1950.

A significant decline in the Index of Consumer Sentiment (ICS) reported by the University of Michigan either preceded or overlapped all 11 American recessions. The 40% drop in ICS ahead of and during the 1980 recession was the largest and the 10% decline during the 1960 recession was the smallest.

There have been periods when ICS fell more than 10% with no recession.

Consumer Sentiment (ICS) fell by 37.9% from June 2021 to August 2022.

2 years later, NBER has NOT declared there was a recession in 2021-2022.

The June\ 2021-August 2022 period qualifies as a vibecession – a significant fall in consumer sentiment NOT accompanied by an economic recession.

I propose the following Scanlon-Sayeed rule (for nerd eyes only; non-nerds can skip it) to determine when the American economy is in a state of vibecession:

The United States is in a state of vibecession when there is a significant decline of at least 20% over a period of 3 years or less in the 3-month average of the ICS reported by the University of Michigan IF the NBER Business Cycle Dating Committee has NOT announced that an economic recession has occurred. A vibecession is over when the 3-month average for ICS reaches an identifiable trough marked as the starting point of a subsequent rise of at least 10% or a period of 12 months when ICS never falls back below that trough. If NBER later announces that an economic recession occurred either during the period of ICS decline or that the recession began within 12 months after the ICS trough, the vibecession declaration shall be nullified by NBER’s recession call.

I’m sorry if that long definition put you to sleep. Stick with me as I explain how:

the vibecession concept fits the economy over the past few years

the 2021-22 vibecession and the weak vibecovery since then threaten Kamala Harris’ chances to be president

Consumer sentiment during the Trump presidency

Americans oozed positive economic vibes when Donald Trump was President – until the covid crisis hit. In October 2016 just before Trump was elected, the Index of Consumer Sentiment (ICS) was just above its long-term average level of 86. By spring 2018, ICS hit 100 – a level not seen since the Clinton presidency.

(For nerd eyes only: throughout this article, I am using 3-month averages of the monthly ICS numbers reported by the University of Michigan. Why 3-month averages? For the same reason that Claudia Sahm uses 3-month averages of the unemployment rate in her Sahm rule designed to give early warning of recessions. 3-month averages smooth out some of the “noise” or variability in monthly survey data that may not always reflect underlying trends.)

ICS stayed in the 90s for the rest of 2018 and throughout 2019 before hitting 100 again in February 2020, the month before covid struck America with a vengeance. The covid crisis knocked consumer sentiment back 26% to 76.1 by June 2020.

In June 2020, NBER declared that the American economy was in recession after peaking in February. NBER subsequently identified April 2020 as the recession trough based on a 19% decline in real GDP, the associated rise in unemployment from 3.5% to 14.8%, and other signs of economic decline.

Economic vibes plunged in 2020 with good reason. The job market and the rest of the economy were depressed. In the spring of 2020, there was a recession throughout the economy, not just a purely mood-based vibecession.

The 26% drop in consumer sentiment was not at all unusual during an economic recession. In fact, the sentiment fall during 2020 represents the median ICS decline out of 11 American recessions since 1950. The median was in line with the average. What was unusual during the 2020 covid recession was how quickly consumer sentiment plunged — the steepest 4-month decline in ICS history dating back to 1952.

Spring 2020 to spring 2021: weak vibe recovery

In the 2nd half of 2020, consumer sentiment first stabilized and then recovered with the rest of the economy to end the year about 80. Sentiment continued rising over the 1st half of 2021 to reach 85 in June 2021. ICS was up more than 15% from the low level of the 2020 covid recession, but still just below the long-term average level of 86.

Normally, the rebound in consumer sentiment after a recession is correlated with the decline before and/or during the recession. For example, of the past 11 recessions, the sentiment fall in 1960 of 10% was the smallest. The subsequent 11% sentiment rebound was also the smallest post-recession rise, but enough to bring ICS back to 99.9 – a hair below the pre-recession peak of 100.

The recovery in consumer sentiment after the 2020 recession was quite different in this respect. ICS plunged by almost 26% from February to June 2020, but crawled back only 15% over the next year to June 2021. After the covid recession, the relatively sluggish rebound brought ICS back to only 85.6 - well below the pre-recession peak of 100 recorded in February 2020.

Vibecession without recession – June 2021 to August 2022

In the summer of 2021, ICS started falling again to less than 70 by year-end. ICS continued plunging to an all-time low of 53.2 in August 2022. From peak to trough, ICS fell 38% in just 14 months– the steepest fall ever in such a short time.

The vibecession was not a mass hallucination of negative sentiments completely unmoored from economic reality. There was no recession. But, by some measures, the post-covid economy in 2022 was not “okayish”.

For example, GDP fell by 0.6% (or by 1.3% at an annual rate) in inflation-adjusted or real terms in the 1st half of 2022. The American economy in early 2022 fit Claessens and Kose’s:

“practical definition of recession, two consecutive quarters of decline in a country’s real (inflation-adjusted) gross domestic product (GDP)—the value of all goods and services a country produces … this definition is a useful rule of thumb”

However, these International Monetary Fund economists go on to explain that defining recession by looking at GDP alone “has drawbacks”.

To call an American recession, NBER economists look at:

“economy-wide measures of economic activity… a range of monthly measures of aggregate real economic activity”

NBER has never declared a recession for a period when jobs are rising and the unemployment rate is falling. Even with real GDP and real personal income both falling, the number of non-farm jobs rose by 1.7% in the 1st half of 2022. The unemployment rate fell from 4% in January 2022 to 3.6% in June.

As a result, NBER has not yet announced that there was a recession in 2021 or 2022. At this late date, the chances of the NBER doing so are even tinier than Green candidate Jill Stein’s chances of winning the election.

In other words, Kyla Scanlon was right on the money with her 2022 vibecession call. ICS plunged to an all-time low that summer without an economic recession.

Why were Americans so gloomy about the economy?

If almost all ready and able Americans were working and there was no recession, why did consumer sentiment plunge 38% from 85 in the summer of 2021 to an all-time low just above 50 one year later?

One possible answer jumps out of the economic data. The 2021-22 vibecession coincided with a rapid burst of inflation. The annual rate accelerated from 1.4% in January 2021 to 7% by year-end. Surveys show that most people hate price inflation even when their wages are keeping pace.

August 2022: Vibecession bottoms and vibecovery starts

By June 2022, annual inflation hit 9.1% – the highest rate in 40 years. This bad news was reported in mid-July. It’s no coincidence consumer sentiment fell that month to the lowest level ever since UMichigan began reporting ICS in 1952.

In the next 12 inflation reports, the annual rate fell each and every month all the way back down to 3% for June 2023. After hitting an all-time low in summer 2022 when inflation peaked, consumer sentiment bounced back by 20% by the summer of 2023 as the annual inflation rate fell.

We need a true statistician of public opinion to prove it. But, I am certain that:

rising inflation caused the June 2021-August 2022 vibecession

falling inflation triggered the vibecovery after August 2022

As measured by consumer sentiment, vibes bottomed in August 2022. A vibecovery – declared by me after the fact of a 10% rise in consumer sentiment following a recession-free vibecession – started after the consumer sentiment trough. ICS rose by almost 50% from 53.2 in August 2022 to 78.5 in April 2024. However, the vibecovery has not so far been strong enough to bring consumer sentiment back to the June 2021 peak of 85 before the vibecession just as the rebound in sentiment after the 2020 covid recession was not strong enough to bring sentiment back to the pre-recession peak of 100 in February 2020.

Has the US slipped back into vibecession in 2024? NO

Since April, the Index of Consumer Sentiment (ICS) has dipped by 3% to a 3-month average of 75.9 in September.

It is theoretically possible that another vibecession has started. However, if you accept my definition, we cannot declare a new vibecession unless:

ICS measured as the 3-month average falls at least 20% below the April 2024 peak of 78.5 to 62.8 on or before April 2027; and

ICS measured as the 3-month average does NOT surpass the April 2024 peak of 78.5 during this period, which would reset the calculation clock; and

NBER does not declare an economic recession either during the period of ICS decline or for 12 months after ICS reaches a new trough.

My best guess is that the small drop in ICS since April 2024 is temporary.

Vibes may get a lift from falling inflation news

For the public, inflation has been the top economic issue since 2021. Sentiment fell as the inflation rate rose in 2021 and the 1st half of 2022. ICS rebounded as inflation fell in the 2nd half of 2022 and 2023. The annual rate was then stuck in a 3.0%-3.7% range from June 2023 to June 2024. The revival in consumer sentiment stalled this spring.

Good economic news may push consumer sentiment back above the 2024 high reached in April. Public perception of inflation data may be influenced by left-digit bias – e.g., a mistaken view that the fall in inflation from 3.0% in June 2024 to 2.9% in July was much better news just because the first digit dropped from 3 to 2 than the previous decline to 3.0% in June from 3.3% in May when the first digit stayed at 3.

The latest announcement that annual inflation fell to 2.5% in August 2024 reinforces the earlier good news that the annual rate starts with 2.

And, more good news is likely on the way with the Cleveland Fed "nowcasting" that inflation will be down to 2.3% in the last pre-election data release on October 10th.

Other economic indicators will not get in the way of the good inflation news. True, 4.2% unemployment is up from the 3.4% rate in April 2023. But, surveys show that most Americans do not care about unemployment unless they are unemployed themselves. Unemployment may not affect consumer sentiment until the rate hits 5%, which is unlikely to happen in 2024. The Harris campaign will not be hurt nor will Trump be helped by more unemployment news unless the Bureau of Labor Statistics report on Friday, November 1st is very bad indeed.

Where is consumer sentiment now?

Over 4 years, Americans rode a vibe roller-coaster. Sentiment plunged during the 2020 recession, climbed after economic recovery to mid-2021 only to plunge again during the inflation-induced vibecession of 2022, which was followed by the modest vibecovery of 2023.

The current stall in consumer sentiment at a relatively low level can be thought of as a vibe hangover after a rapid succession of ups and downs.

The September reading for the Index of Consumer Sentiment (ICS) is 77.3. (Monthly ICS, not 3-month average, and adjusted by me to be comparable to historical ICS data prior to the April 2024 transition to a web-based survey from phone-based.)

Weak vibes and presidential elections

With sentiment at similar levels before the 1980 and 1992 elections, Presidents Carter and Bush the Elder lost decisively. No party has retained the White House with ICS below 82.6 when President Obama was re-elected in 2012.

Another way to look at that record is that no out-of-White-House party has ever lost a presidential election with consumer sentiment as low as it is today. The vibecession and weak vibecovery opened the White House door wide open for the Republican Party. Had Republican voters nominated a candidate focused on tapping Americans’ economic discontent, Kamala Harris would have no chance to be elected. If Trump and his team had copied Ronald Reagan’s 1980 playbook and focused their campaign on the economy, Harris would be way behind now.

Instead, the race was balanced on a knife edge before the debate last Tuesday. Trump’s mad behavior is the only reason the race was close before the debate. Trump’s terrible, horrible, no good, very bad debate performance may adversely affect his support levels in post-debate polls to the point that even an Electoral College victory may start to look less likely.

The vibecession and weak vibecovery should have handed Donald Trump an easy election victory in 2024. So far, Trump has not done enough to exploit economic discontent. He may still win the election. But, if the Donald does go on to lose, the words of James Carville and Kyla Scanlan can be combined to form the epitaph for Trump 2024 : “It should have been about the economic vibes, stupid candidate!”