Fed a bit player until Carter picked Volcker

Hinge moment in US economic history would not have occurred without Jimmy Carter.

From left: Paul Volcker, President Carter, G. William Miller Photo credit: Associated Press

Respectful takes honoring Jimmy Carter

Inflation ended Carter’s presidency, even though Carter appointed Federal Reserve Chair Paul Volcker, the man who ended high inflation.

Before Volcker, Milton Friedman on the right and JK Galbraith on the left agreed that Fed Chair was “not a terribly important job”.

Volcker’s predecessor G. William Miller volunteered to move from Fed Chair to what he thought would be a better job – Treasury Secretary.

Since Volcker, Fed Chair has been “the 2nd most powerful person in government”.

Unlike Carter, President Trump got his first Fed Chair pick right when he promoted Jerome Powell in 2018.

Trump has soured on Fed Chair Powell and vows to find a replacement when Powell’s term expires in 2026.

The most important economic decision of Trump 2.0: the next Fed Chair.

We can only hope that Trump will do as good a job as Carter did picking his second Fed Chair.

Carter: Exceptional post-president, unlucky president

President Jimmy Carter is an inspiration to anyone who has suffered a mid-life crisis triggered by career failure. Carter left the White House at age 56 in 1981 after experiencing the 2nd-worst defeat ever (in Electoral College points) of any US president running for re-election.

Widely derided as an ineffective scold and shunned as a loser by his own Democratic Party, a lesser man might have fallen into a paralyzing depression. Instead, Carter devoted the rest of his life to service. His post-presidency contributions – e.g., organizing the drive to stamp out Guinea worm disease – were greater than even his notable achievements as president – e.g., Egypt-Israel deal.

Eulogists lamented Carter’s bad luck in office:

“He was a very good man, but an unlucky president.” (Paul Krugman)

“He was an unlucky president… We are lucky to have had him.” (James Fallows)

Inflation helped Reagan defeat Carter in 1980

Krugman summarized Carter’s bad luck presiding over bad economic times:

“the great productivity boom … had sputtered out, for reasons we still don’t fully understand …oil shocks had a much bigger effect on inflation than comparable shocks would today… persistent inflation before Carter took office … had made the economy vulnerable to wage-price spirals…So inflation exploded, and Carter lost the election with a sense that his management of the economy had failed”

The great irony is that Carter appointed Federal Reserve Chair Paul Volcker – the man who killed high inflation. Unluckily for President Carter, Volcker’s tight monetary policy had only just started to work on inflation by voting day in 1980.

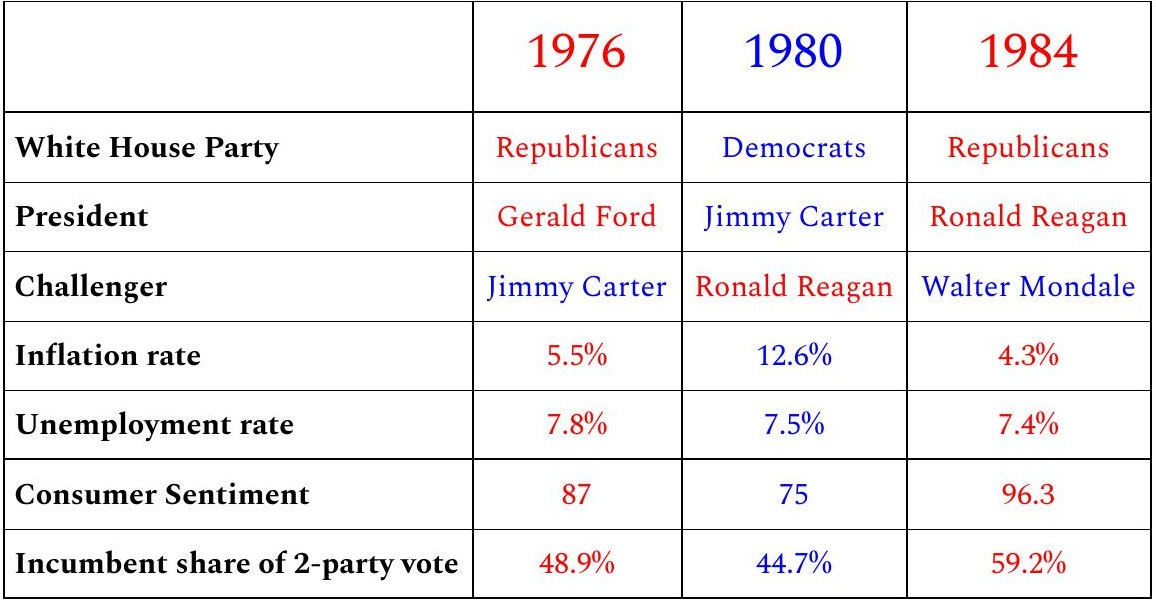

The table below compares unemployment, inflation, consumer sentiment and incumbent presidents’ fates in the 1976, 1980 and 1984 elections.

Sources: University of Michigan Index of Consumer Sentiment (ICS) in October just before each November election. Bureau of Labor Statistics for inflation and unemployment rates.

Notes: Inflation and unemployment rates shown in this table are the last data reported before November election day – September in all cases except October 1984 unemployment rate. This differs from other election comparisons in some of my other posts using November data consistent with Professor Justin Wolfers’ approach. Incumbent party share of the 2-party vote is a better measure than share of total votes including minor parties.

Unemployment was about the same before all 3 elections. What differed was inflation and consumer sentiment – the best measure of how Americans feel about the economy and the President’s economic management. My table is not proof beyond a reasonable doubt for statisticians. But, the comparison indicates strongly that high inflation killed Carter’s re-election chances in 1980 and that the subsequent fall in inflation under Fed Chair Volcker guaranteed Ronald Reagan’s re-election in 1984.

How did Carter choose Volcker?

So far, I’m just retelling a tale that everyone knows. My trip back in time is worth taking for a closer look at Carter’s Fed Chair appointments:

1978: G. William Miller replaces Nixon appointee Arthur Burns

1979: Volcker replaces Miller who resigned to become Treasury Secretary

We can draw some lessons from Carter’s initial mishandling of the Fed for President Trump’s economic team as they consider replacements for Jerome Powell whose term as Fed Chair expires in May 2026.

Looking back from 2025, it seems astounding that when President Carter asked Fed Chair G. William Miller to take over as Treasury Secretary in 1979, Miller jumped at the chance to move to what he believed would be a better job.

The Mu$eum of American Finance (a Smithsonian affiliate) calls the Fed Chair:

“the second most powerful person in the US government, after the President. That is because the Chairman leads a central bank that sets US monetary policy, supervises and regulates the nation’s banks, oversees a vast payments system that most Americans use almost daily and cooperates with foreign central banks to promote international financial stability.”

Only the first Treasury Secretary Alexander Hamilton from 1789 to 1795 could ever have been considered “the second most powerful person in the US government”. Why did Miller think so little of being Fed Chair that he was happy to trade in that job to be Treasury Secretary?

Miller’s dim view of his job as Fed Chair was the consensus opinion at the time. The Federal Reserve was held in such low esteem in the 1970s that conservative economists Milton Friedman and Alan Greenspan had the same reaction as liberal economist John Kenneth Galbraith to Miller’s selection.

“On very few occasions in the past has the name of the man who is chairman of the Fed made much difference.” (Friedman)

“it's not a terribly important job.” (Galbraith)

“Critics of the Fed impute a degree of efficacy to the institution which really isn't there. The policy range is much smaller than most people imagine.” (Greenspan)

The sentiment that the Fed wasn’t important may have lulled Carter and his team into the mistake of making Miller Fed Chair in the first place. Carter had run for president as an “outsider”. He may have liked the notion of sending in Miller, head of the manufacturing conglomerate Textron, as a fellow “outsider” to run the Fed. No one considered whether Miller’s minimal exposure to financial industry issues might hinder his effectiveness in what was “not a terribly important job.”

Miller didn’t get along with the other Governors during his year and a half at the Fed. They ignored his no-smoking rule and his 3-minute limit on speaking time at Board meetings. Despite the wisdom of Miller’s new rules, his new colleagues didn’t respect him enough to comply. Miller’s status as Chair in name only became publicly known when Governors on the Federal Open Market Committee voted to raise the short-term interest rate with Miller voting no.

Fed Chair Miller was far from being the “second most powerful person in the US government”. He couldn’t even enforce rules to conduct Board meetings, let alone stop an interest rate increase. Miller remained an outsider throughout his time as Fed Chair and was relieved to be promoted to Treasury Secretary.

It was Paul Volcker who transformed being Fed Chair into the “second most powerful person in the US government”. When Volcker took over in August 1979, inflation was perceived to be an unstoppable force beyond the Fed’s control. The annual rate had risen by fits and starts from under 2% in 1965 to 11.8%. When Volcker left the Fed in August 1987, inflation was down to 4.3% and had been under 5% for almost 5 years.

Was Carter’s choice of Volcker an accident?

Yes, in a narrow sense. But, no if we take a more generous view of the events.

Volcker was not Carter’s first choice. So, yes, Fed Chair Volcker was an accident of history in the narrow sense of not being the President’s first choice.

But, there was more to the story than economic historian Brad DeLong’s portrayal of President Carter signing off on a name put in front of him without knowing much about Volcker.

“Carter was running a disorganized White House… There was no obvious replacement at hand. Carter grabbed the most senior … Federal Reserve official … Paul Volcker – and made him Federal Reserve Chair.”

In a nytimes.com interview, DeLong faulted Carter’s Director of Domestic Policy Stuart Eizenstat for not properly vetting Volcker.

“Charlie Schultze again asked Carter’s domestic policy adviser, Stu Eizenstat, if anyone had done any research into what Paul Volcker’s views about monetary policy should be and as I understand it, did not get an answer. And so Paul Volcker winds up as Carter’s choice for Federal Reserve chair”

Eizenstat himself told a different story in his memoir of 4 years in Carter’s White House. Eizenstat wrote that Carter’s economic team compiled a list of candidates including Volcker, who had also been on the short list when Miller was selected.

To replace Miller, Carter asked David Rockefeller to take the Fed job. Rockefeller declined and recalled in his memoirs:

I would have been responsible for implementing a set of draconian policies to wring inflation from the economy and stabilize the dollar. As a wealthy Republican with a well-known name, it would have been extremely difficult for me to make the case for tight monetary policy and sell it to a skeptical Congress and an angry public.

Next on the list: Bank of America President Tom Clausen. Clausen’s wife exercised her right to veto the move.

Carter then discussed the Fed job with Bruce MacLaury, head of the Brookings Institution think tank, without landing MacLaury.

Despite their clashes at the Fed, Miller favored Volcker and persuaded Carter to meet him. Volcker got the job even though he left the White House thinking that he’d botched the interview.

“I was kind of an ass, because I did all the talking …he (Carter) isn’t going to hire me…I blew it. I said that I attached great importance to the independence of the Federal Reserve and that I also favored a more restrictive monetary policy. And just for emphasis I pointed at Miller … and added that I wanted a tighter policy”.

Volcker was not first on the list of candidates. But, Carter and his team did due diligence before appointing Volcker as Fed Chair. Carter knew how Volcker would approach the job. Volcker told Carter so during the job interview. Carter’s decision to appoint Volcker was NOT an accidental outcome of White House bumbling.

What was a happy accident was Carter’s decision to move Miller to Treasury. Carter effectively gave himself a do-over after making the mistake of appointing Miller as Fed Chair in 1978. Miller couldn’t communicate Fed policy. He doubted that raising interest rates to control inflation would be worth the cost in lower employment and growth. Inflation rose from 6.6% when Miller arrived at the Fed in March 1978 to 11.8% when he left in August of the following year.

Bringing in an outsider to shake up an organization is a common practice in government, business and the non-profit sector. Leading monetarist Milton Friedman was so fed up with the Fed that he praised Carter’s pick of Miller.

“Money is too important a matter to be left to bankers.”

Carter and Friedman were both wrong in this particular case. Parachuting in an outsider to take charge works if the new boss can articulate clear goals and plans. G. William Miller was not the right person for the Fed Chair job (even if he was certainly right about no-smoking).

I do not suggest that Jimmy Carter could have saved his presidency if he had installed Volcker as Fed Chair in 1978 instead of Miller. The recession-in-two-installments of 1980-82 triggered by Volcker’s high interest rates would have arrived earlier. Had Volcker taken charge in 1978 instead of 1979, inflation might have been a bit lower than turned out to be the case by the November 1980 election, but unemployment might well have been higher. Unforgiving voters would still have blamed Carter for not fixing the bad economy that he inherited from the previous administration.

Reagan would have been elected in 1980 and re-elected in 1984. Carter’s mistake installing Miller as Fed Chair in 1978 did not change the course of US history or even Carter’s life. But, the 5 years from 1978 through 1982 – the worst years for the US economy since the Great Depression of the 1930s – might have been not quite so bad.

Implications for Trump 2.0

What can the Trump economic team learn from Carter’s Fed appointments?

When it comes to picking a Fed Chair, Donald Trump is already ahead of Jimmy Carter. Both Trump and Carter decided against reappointing the Fed Chair installed by a previous president from the other party. President Carter was lucky to get two swings to connect the right candidate to the Fed Chair job. Trump got it right the first time. His decision to install “insider” Jerome Powell as Fed Chair in 2018 worked out much better than Carter’s selection of “outsider” G. William Miller 40 years earlier.

However, President Trump quickly soured on Powell. Trump called Powell an enemy and said that he will not reappoint Powell when his term as Fed Chair ends in 2026.

Choosing the next Fed Chair will be the most consequential economic policy decision of Trump’s 2nd term. The risk to the US economy is that Trump will flip Carter’s script. Carter’s Fed Chair picks were outsider Miller, a good person who never got the hang of the job, followed by capable insider Volcker. Trump tried capable insider Powell and now wants someone better. For his 2nd term team, Trump has favored many outsiders – e.g., Gabbard, Hegseth, RFK Jr., Dr. Oz, Patel. If Trump picks someone of that ilk as Fed Chair, Americans will pay the price for years to come.

Memories of a longer Ford administration

(that might have been)

Jimmy Carter won the 1976 election narrowly. How would US economic and political history have unfolded if Republican President Gerald Ford had won?

Ford would likely have kept Nixon appointee Arthur Burns for another term as Fed Chair. Republican Burns might well have continued his approach of limiting interest rate increases for fear of damaging his party’s popularity.

The US economy would have puttered along. Inflation would have climbed to the same heights reached during the Carter administration or perhaps even higher.

Reagan might well have been the Republican candidate in 1980. But, even the Great Communicator might have struggled to separate himself from Ford’s unpopularity. Walter Mondale or another Democratic candidate would likely have won in 1980.

It’s very unlikely that Paul Volcker would ever have been Fed Chair in this scenario. Perhaps Mondale or another hypothetical Democratic winner of the 1980 election would have found a better Fed Chair capable of reducing inflation gradually with a shallower recession than occurred under Volcker. But, it’s also possible in this scenario that the Fed would have continued as an economic policy backwater. Successive Democratic and Republican administrations might have settled for high and persistent inflation for many more years to come.

Inflation killed Carter’s re-election chances in 1980, but Carter’s victory in 1976 was a necessary step on the road to Fed Chair Paul Volcker and the end of high inflation.

Agreed about surprising nature of Friedman comments to NY Times at 1977 American Economics Association meeting shortly after White House announced Miller's appointment as Fed Chair. I think you are right, Rod, that Friedman partly meant that Fed Chair just has one vote. I'm just guessing that he was also partly being provocative and partly expressing his frustration that the Fed had allowed inflation to rise and not adopted Friedman's idea to fix money supply growth at some low and constant level. Fed Chair just one vote on a Committee, but I think Friedman may have leveled harsh words at outgoing Arthur Burns during Burns' time as Fed Chair. I'm returning 2 Volcker bios to library today. Bio by William Silber has long section about Friedman's criticisms of Volcker for not setting a money supply growth target.

I had no idea that Milton Friedman regarded the job of Federal Reserve Chair as not very important. If "inflation is everywhere and always a monetary phenomenon" (if I got that roughly right), he must've thought that the Fed itself was important. Was the idea just that the Chair was first among equals, and just one member of the Federal Open Market Committee who could be outvoted?